The Gardens at Market Square development in the Central Business District; Photo: Connie Zhou, courtesy of Piatt Companies

The Truth About Tax Diversions

Clearing up common misconceptions about TIF & TRIDs

Tax diversion programs, such as Tax Increment Financing (TIF) and Transit Revitalization Investment Districts (TRIDs), are critical public financing tools administered by the Urban Redevelopment Authority of Pittsburgh (URA) in the City of Pittsburgh to unlock development sites that are not financially feasible without public funding. These development sites involve extraordinary costs to remove barriers to new development, such as inadequate infrastructure, environmental contamination, and other site-specific conditions that must be addressed.

For development to occur, developers that are seeking tax diversion funding must commit to substantial private investment in their development, investment in necessary public infrastructure, and to working with the URA to request the three taxing bodies – Allegheny County, City of Pittsburgh, and Pittsburgh Public Schools – agree to authorize a tax diversion, through legislation such as an ordinance or resolution.

A tax diversion means a percentage of future tax revenue resulting from a private development (that otherwise would not occur if not for the TIF/TRID) will be diverted, in part, to pay for necessary public infrastructure and improvements within the boundaries of a designated tax diversion ‘district,’ or geographic area as defined by legislation.

Emphasizing Interdependency

- The guaranteed future increased tax revenue from a large-scale private development is what makes a tax diversion possible to fund public improvements; and

- The tax diversion toward public improvements is what makes the development financially feasible for the developer.

This mutual reinforcement is what makes the development of the property possible, otherwise it would remain underutilized and generate less taxes for the three taxing bodies.

The URA underwrites, analyzes, implements and monitors TIFs, TRIDs, and other tax diversion tools on behalf of the three taxing bodies in Pittsburgh. Our staff critically review and evaluate all applications to ensure that ‘but for’ the tax diversion, the project would not otherwise happen, that there is significant public and private investment leveraged into the project, that the public monies generated by the TIF/TRID only pay for public infrastructure and eligible expenses, and that the TIF/TRID projects are compliant with tax diversion state and local statutes.

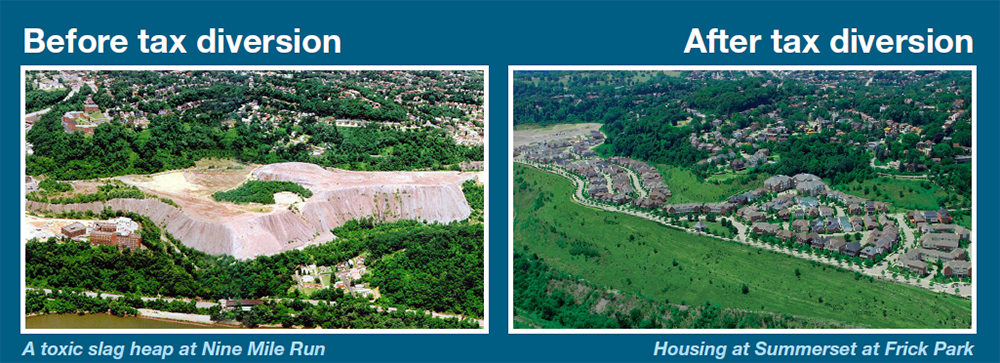

The URA has completed successful TIF districts and TRIDs throughout the City, including at the Southside Works, Pittsburgh Technology Center, Summerset at Frick Park, and Gardens at Market Square, among others. Tax diversion tools enabled the URA and partners to completely transform these districts, helping Pittsburgh restore land to a higher productivity and reposition the post-steel economy for a better future.

Explore five truths about tax diversion tools to better understand what they are.

Tax diversions are not a “tax break” for developers and do not take taxes away from the taxing bodies.

A developer is required to continue to pay taxes on the full assessed value of the property, so the County, City, and School District continue to receive the annual tax revenue they had been receiving before a project began. The new development increases the taxable value of the site. When a tax diversion project is completed and reassessed, or completed and operational, a percentage of the new taxes is distributed to the taxing bodies, while another percentage of ‘pledged’ taxes are used to repay the debt from public improvements for a set period of time. Upon full repayment of all of the debt used for the public improvements, the taxing bodies will receive the full additional tax revenue resulting from the development.

Tax diversions benefit both residents and private developers.

While Pennsylvania law allows for TIF and TRID funds to be applied toward private development, local ordinances require that diverted taxes be used for public infrastructure improvements such as streets, sidewalks, streetlights, sanitary sewer and water lines, public use facilities, parks and public green space, parking structures, and more. The funds can also be used toward affordable housing and site preparation costs.

Members of the public have opportunities to provide input on the TIF and TRID planning process.

The statutes governing TIF and TRIDs require public hearings and opportunities for public engagement over a minimum of six months. The URA must present to the three taxing bodies at their regular scheduled meetings for a TIF district or TRID to be approved.

Tax diversions administered by the URA are not a “slush fund.”

The uses of TIF and TRID funds are explicitly spelled out in established 'implementation plans' adopted by the taxing bodies for each project. These plans are the basis for the creation of a TIF district and/or TRID.

Tax diversions help the URA and developers successfully compete for state and federal dollars.

Using TIF and TRID funding shows state and federal agencies, as well as private foundations and investors, that the local government supports the project and is willing to invest local funds for economic development.